Business

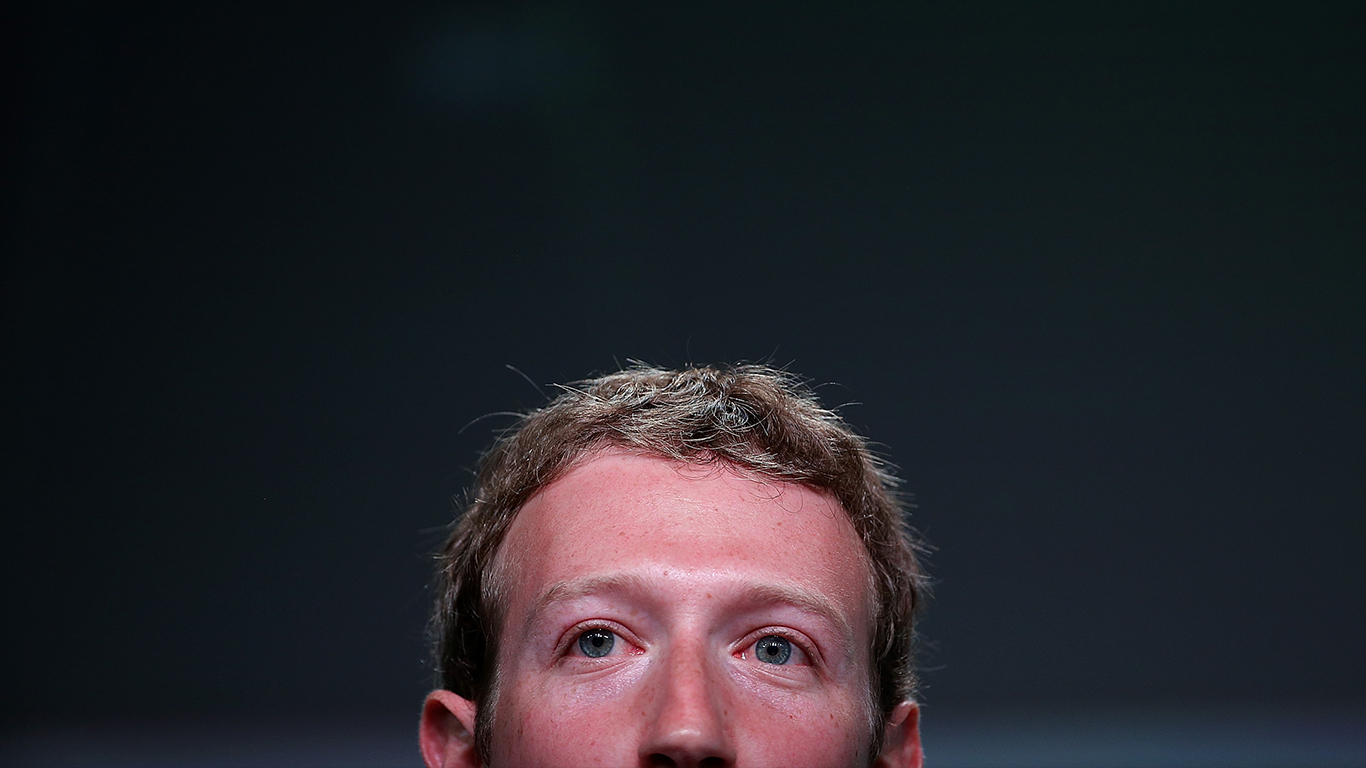

Meta’s Stock Recovery: Is Now the Time to Invest Below $650?

Meta Platforms (NASDAQ:META) has experienced significant fluctuations in its stock price, recently recovering to around $650 after dipping below $600. This recovery follows a strong performance in its third-quarter earnings for 2025, where revenue reached $51.24 billion, reflecting a 26.2% increase year-over-year and surpassing analyst expectations by 3.71%. Despite these positive financial results, the company’s cash per share has fallen dramatically, down 76.74% from the previous year, as Meta prepares to invest heavily in artificial intelligence (AI), planning to allocate up to $72 billion in 2025.

The fluctuations in Meta’s stock can be traced back to its strategic pivot towards AI, a move initiated by CEO Mark Zuckerberg. The company faced declining user growth and revenue from its Family of Apps segment, which includes Facebook, Instagram, WhatsApp, and Messenger. This downturn saw the stock plummet below $90 in late 2022. However, with the rise of AI tools such as ChatGPT, Meta’s fortunes began to change, leading to a more favorable stance from Wall Street.

Despite the promising growth, the stock’s recent performance suggests a more cautious outlook from investors. After reaching a peak near $785, Meta’s stock has struggled to maintain upward momentum, remaining relatively flat over the past six months. This stagnation may indicate that investors are hesitant to assign a higher valuation to the stock until the benefits of the substantial AI investments become clearer.

Zuckerberg’s commitment to AI represents a bold gamble that contrasts sharply with past strategies focused on Reality Labs, which had not gained investor confidence. While the AI initiative has already shown some positive results in enhancing advertising through improved targeting, it remains to be seen whether these advantages will fully offset the considerable costs associated with the investment.

The financial implications of Meta’s AI strategy are noteworthy. As of the first quarter of 2025, the company reported a net cash position of $20.711 billion. However, by the third quarter, the situation shifted as they reported $6.612 billion in net debt, raising concerns about cash flow management. This significant decrease in cash per share, along with increasing debt levels, places additional pressure on the company to demonstrate rapid returns on its AI investments.

Investors are now faced with a critical question: should they buy the dip in Meta’s stock, or consider other options? While the company has shown marked revenue growth, there are arguments against further investment. The current market premium on Meta stock is more than double the levels seen in late 2022, despite the business operating under riskier conditions.

For those looking to capitalize on the AI and advertising synergy, alternatives such as Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL) may present a more diversified investment opportunity. Meanwhile, Microsoft (NASDAQ:MSFT) continues to be a strong contender for those interested in broader AI trends.

In conclusion, while Meta Platforms has made impressive strides in revenue growth and is at the forefront of the AI movement, potential investors should weigh the risks associated with its high debt levels and aggressive spending on AI against the backdrop of a potentially cyclical advertising market. The decision to invest in Meta stock below $650 requires careful consideration of both the immediate financial landscape and the long-term outlook for the technology sector.

USTR Confirms Urgent Agreement on Pharma Pricing with UK

U.S. Negotiators Visit Russia to Advance Peace Talks on Ukraine

Child Protection Services Overwhelmingly Target Families of Disabled Kids

Detroit Catholic Central Wins Division 1 State Title with 42-19 Victory

Trump Administration Initiates Major Changes to SNAP Eligibility

Meta’s Stock Recovery: Is Now the Time to Invest Below $650?

CD Projekt Red Confirms No Release for The Witcher 4 in 2026

Black Friday 2025: Record Online Sales Surge Amid Store Decline

Urgent: Jim Chanos Warns of Nvidia’s Risky Debt Market Amid Market Volatility

Urgent Update: Tom Aspinall’s Vision Deteriorates After UFC 321

MIT Scientists Uncover Surprising Genomic Loops During Cell Division

University of Hawaiʻi Joins $25.6M AI Project to Enhance Disaster Monitoring

AI Disruption: AWS Faces Threat as Startups Shift Cloud Focus

Time Crystals Revolutionize Quantum Computing Potential

Honeywell Forecasts Record Business Jet Deliveries Over Next Decade

Discover the Full Map of Pokémon Legends: Z-A’s Lumiose City

GOP Faces Backlash as Protests Surge Against Trump Policies

Parenthood Set to Depart Hulu: What Fans Need to Know

-

Top Stories1 month ago

Top Stories1 month agoUrgent Update: Tom Aspinall’s Vision Deteriorates After UFC 321

-

Health2 months ago

Health2 months agoMIT Scientists Uncover Surprising Genomic Loops During Cell Division

-

Science4 weeks ago

University of Hawaiʻi Joins $25.6M AI Project to Enhance Disaster Monitoring

-

Top Stories2 months ago

Top Stories2 months agoAI Disruption: AWS Faces Threat as Startups Shift Cloud Focus

-

Science2 months ago

Science2 months agoTime Crystals Revolutionize Quantum Computing Potential

-

World2 months ago

World2 months agoHoneywell Forecasts Record Business Jet Deliveries Over Next Decade

-

Entertainment2 months ago

Entertainment2 months agoDiscover the Full Map of Pokémon Legends: Z-A’s Lumiose City

-

Top Stories2 months ago

Top Stories2 months agoGOP Faces Backlash as Protests Surge Against Trump Policies

-

Entertainment2 months ago

Entertainment2 months agoParenthood Set to Depart Hulu: What Fans Need to Know

-

Politics2 months ago

Politics2 months agoJudge Signals Dismissal of Chelsea Housing Case Citing AI Flaws

-

Sports2 months ago

Sports2 months agoYoshinobu Yamamoto Shines in Game 2, Leading Dodgers to Victory

-

Health2 months ago

Health2 months agoMaine Insurers Cut Medicare Advantage Plans Amid Cost Pressures